The Problem Isn’t the Will. It’s Everything Else.

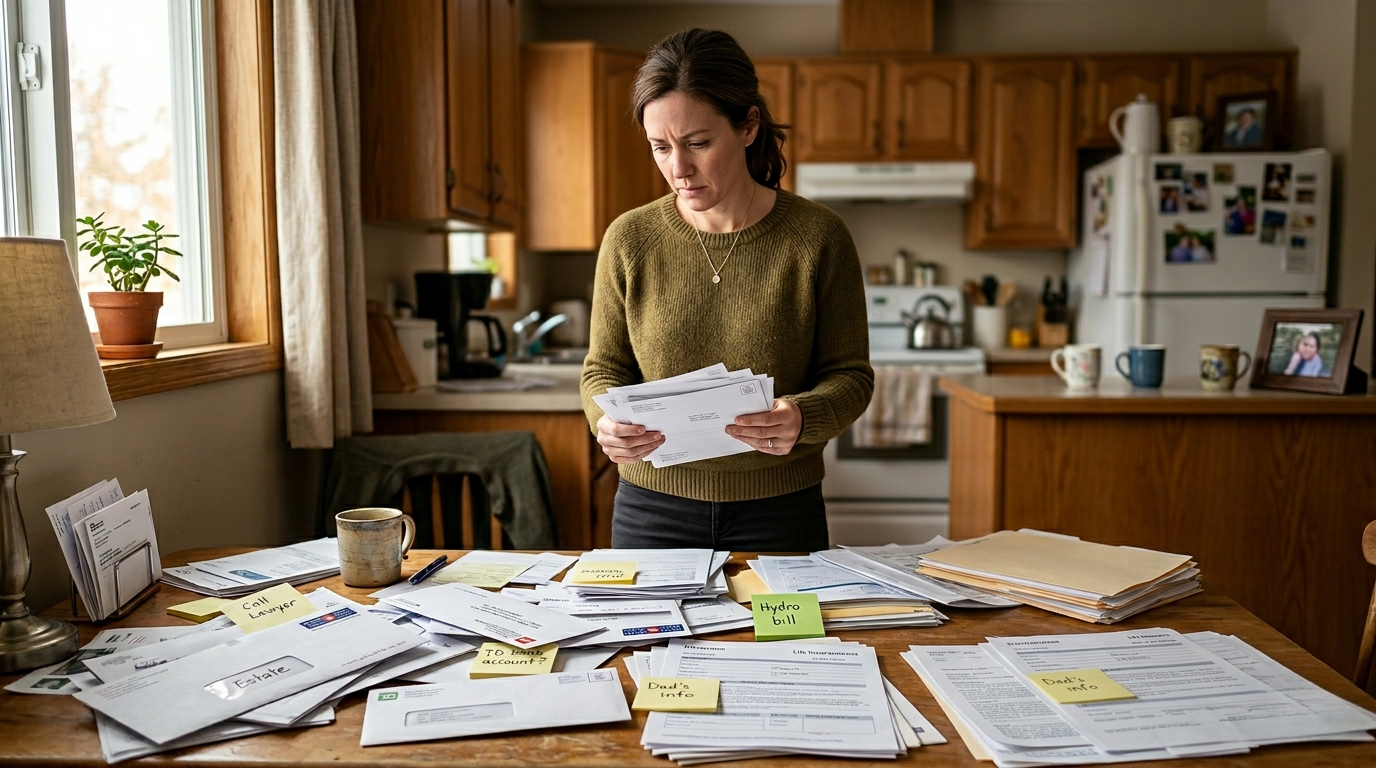

When Priya’s mother passed away in February, she had a will. Signed, witnessed, stored with a lawyer. By every standard measure, her mother had done the right thing. But when Priya showed up at the family home the following week to begin the estate, she stood in the kitchen with a notepad and realized she had no idea where to start. She didn’t know which bank held the chequing account. She couldn’t find the insurance policy. The Rogers bill kept coming but there was no record of the login. The will said what her mother wanted done with her estate. It said nothing about how to find it.

That’s not a planning failure. That’s an organization failure. And we’re learning just how widespread the problem actually is.

What the Numbers Actually Show

The statistics on estate planning in Canada tend to focus on wills. Only about half of Canadians have one. Among millennials the number drops further. These are real gaps.

But here’s what the data also shows: even among Canadians who do have wills, most haven’t had a meaningful conversation with their family about where things are, what accounts exist, or what their wishes look like in practice. A 2025 Willful survey found that while 59 percent of Canadians say they’ve talked about end-of-life wishes, only 36 percent both know their family’s wishes and have actually shared their own. Another survey from the same year found that only a third of respondents had even discussed where they want to spend their final days.

The will gets written. The conversation doesn’t happen. The executor, often a spouse or adult child, inherits a puzzle with half the pieces missing.

What the First Week Actually Looks Like

I’m a Certified Executor Advisor, and I’ve served as an executor myself. Between those two things, I’ve seen this gap from every angle, and I can tell you that the first week of an estate has almost nothing to do with the will.

It often starts with death certificates. Depending on the estate, you may need several, because some institutions want their own original copy. Then comes the list. Which banks? Which accounts? Is there a line of credit? A safety deposit box? A pension that needs to be redirected or cancelled? Subscriptions charging a card that shouldn’t be used anymore? A digital storage account full of photos no one can access because the password died with the person?

The will doesn’t answer any of those questions. A well-organized estate does.

Most executors spend the first two to four weeks just locating things. Not distributing assets, not filing taxes, not dealing with beneficiaries. Just finding the pieces. Every hour spent hunting for a policy number or tracking down a financial institution is an hour of administrative cost to the estate, and an hour of time the executor isn’t getting back.

The family that prepared isn’t spared grief. But they’re spared the chaos that makes grief so much harder to get through.

When Colette’s husband passed away unexpectedly at 61, she found herself executor of an estate she knew almost nothing about. He had handled the finances. She knew roughly what they had, but not where it was held, who their insurance was through, or whether there were accounts she didn’t know about. She spent weeks on the phone, writing letters, and waiting. A year later, she still wasn’t entirely sure she’d found everything. That uncertainty is one of the quieter costs of an unorganized estate.

What Prepared Actually Looks Like

If you’re a homeowner, a parent, a common-law partner, a business owner, or anyone who has people in their life who’d be affected if something happened to you, the question isn’t whether you need a plan. It’s whether your plan is actually findable.

A will in a lawyer’s office is a start. But your executor also needs to know which financial institutions hold your accounts, where your insurance policies are and who to call, what your digital accounts are and how to access or close them, where your important documents are physically stored, who your key contacts are, and what your wishes are for the things a will doesn’t cover.

That’s not a legal document. That’s an organized record. And it’s what makes the difference between an executor who can move forward and one who spends months in a paper chase.

When Tariq’s father died at 78, the family assumed the estate would be straightforward. There was a will, a house, and a modest investment account. What they didn’t have was any record of which institutions held what. Tariq spent weeks making calls, sending letters, and waiting for responses, all while trying to figure out whether there were accounts he hadn’t turned up yet. He never did feel entirely confident the estate was complete. That uncertainty doesn’t go away quickly.

Tools That Close the Gap

This is exactly why I built In Plain Sight™ as part of the NEXsteps planning toolkit. It’s a personal records organizer designed to capture all of it: your accounts, your documents, your digital life, your insurance, your key contacts. Structured so the person who steps in after you can find what they need without turning every drawer inside out. It prints cleanly so your executor can work from a hard copy, and it covers the categories that come up again and again in real estate administration.

For families who want to tackle the full picture, The Prepared Estate™ bundles In Plain Sight with Estate Architect™, a companion tool that walks you through the decisions that shape a complete estate plan before you sit down with a lawyer or an advisor.

Neither tool replaces a will. Neither replaces legal advice. But both address the gap that’s costing Canadian families weeks of confusion and real administrative time, every single day.

Explore In Plain Sight™, The Prepared Estate™, and the full NEXsteps planning toolkit.

Priya’s mother had a will. That was something. But it would have been so much easier, and so much more honouring of everything she built, if she’d left a map alongside it.

Don’t leave a scavenger hunt.

Visit our services page to see how we can help.

Watch our video here, or watch on our YouTube Channel:

Prefer a podcast? Listen here!

Please send us your questions or share your comments.

Disclaimer: This content is for general information only and is not legal, financial, medical, or tax advice.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}